But, based on my conversations with Israeli decision-makers, this period of forbearance, in which Netanyahu waits to see if the West’s nonmilitary methods can stop Iran, will come to an end this December. Robert Gates, the American defense secretary, said in June at a meeting of NATO defense ministers that most intelligence estimates predict that Iran is one to three years away from building a nuclear weapon. “In Israel, we heard this as nine months from June—in other words, March of 2011,” one Israeli policy maker told me. “If we assume that nothing changes in these estimates, this means that we will have to begin thinking about our next step beginning at the turn of the year.”

You would think, as John Bolton does, that Isarel is constrained to make their military move before any plant fueling. But the radiation mess is just one of many messes being weighed into the calculus. So we may not be very well served with this week's fueling schedule as a military schedule.

What is more likely, then, is that one day next spring, the Israeli national-security adviser, Uzi Arad, and the Israeli defense minister, Ehud Barak, will simultaneously telephone their counterparts at the White House and the Pentagon, to inform them that their prime minister, Benjamin Netanyahu, has just ordered roughly one hundred F-15Es, F-16Is, F-16Cs, and other aircraft of the Israeli air force to fly east toward Iran—possibly by crossing Saudi Arabia, possibly by threading the border between Syria and Turkey, and possibly by traveling directly through Iraq’s airspace, though it is crowded with American aircraft.

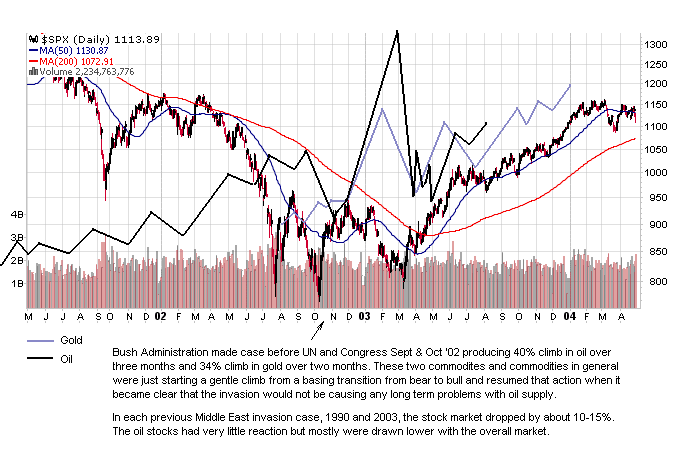

Regardless of when the strike happens, the conscientious investor has to try to anticipate the market implications. You could stay totally out of all markets until a military option is taken. That would have kept you out of the Cold War market from 1957 to 1989. Or you can study what past Middle East blow ups did, and weight portfolios accordingly. If you look at the two most recent Middle East blow ups, Saddam's invasion of Kuwait in August of 1990 and Bush's announcement that we were going to invade Iraq, believed to be chock full of bio and chemical weapons in late 2002, you see that the two beneficiaries are oil and gold. In the 1990 blow up: (click to enlarge charts)

And in the 2002 blow up:

These two time frames were during a bear market in commodities (1990) and a beginning bull market (2002). The geopolitical events caused just a brief detour by gold and oil from the paths they were taking, demonstrating the power of macro-economic trends over geopolitical events. Of course Iran/Israel may be a macro-economic trend changer if it were to occur.

It's worth noting that oil stocks didn't do much over these past shocks, but gold stocks typically did about whatever gold did. So of the four good "shock" investments that come to mind - gold, oil, gold stocks, and oil stocks - we've had 3 up and one down over past shocks.